|

|

|

|

|

|

Short-Range Actuarial EstimatesFor the short-range period (2013 through 2022), the Trustees measure financial adequacy by comparing projected asset reserves at the beginning of each year to projected program cost for that year under the intermediate set of assumptions. Maintaining a trust fund ratio of 100 percent or more — that is, reserves at the beginning of each year at least equal to projected cost for the year — is a good indication that the trust fund can cover most short-term contingencies. The projected trust fund ratios under the intermediate assumptions for OASI alone, and for OASI and DI combined, exceed 100 percent throughout the short-range period. Therefore, OASI and OASDI satisfy the Trustees’ short-term test of financial adequacy. However, the DI Trust Fund fails the Trustees’ short-term test of financial adequacy. The Trustees estimate that the DI trust fund ratio was at 85 percent at the beginning of 2013. After 2013, the projected DI trust fund ratio declines until the trust fund reserves become depleted in 2016. Figure II.D1 shows that the trust fund ratios for the combined OASI and DI Trust Funds decline consistently after 2010.

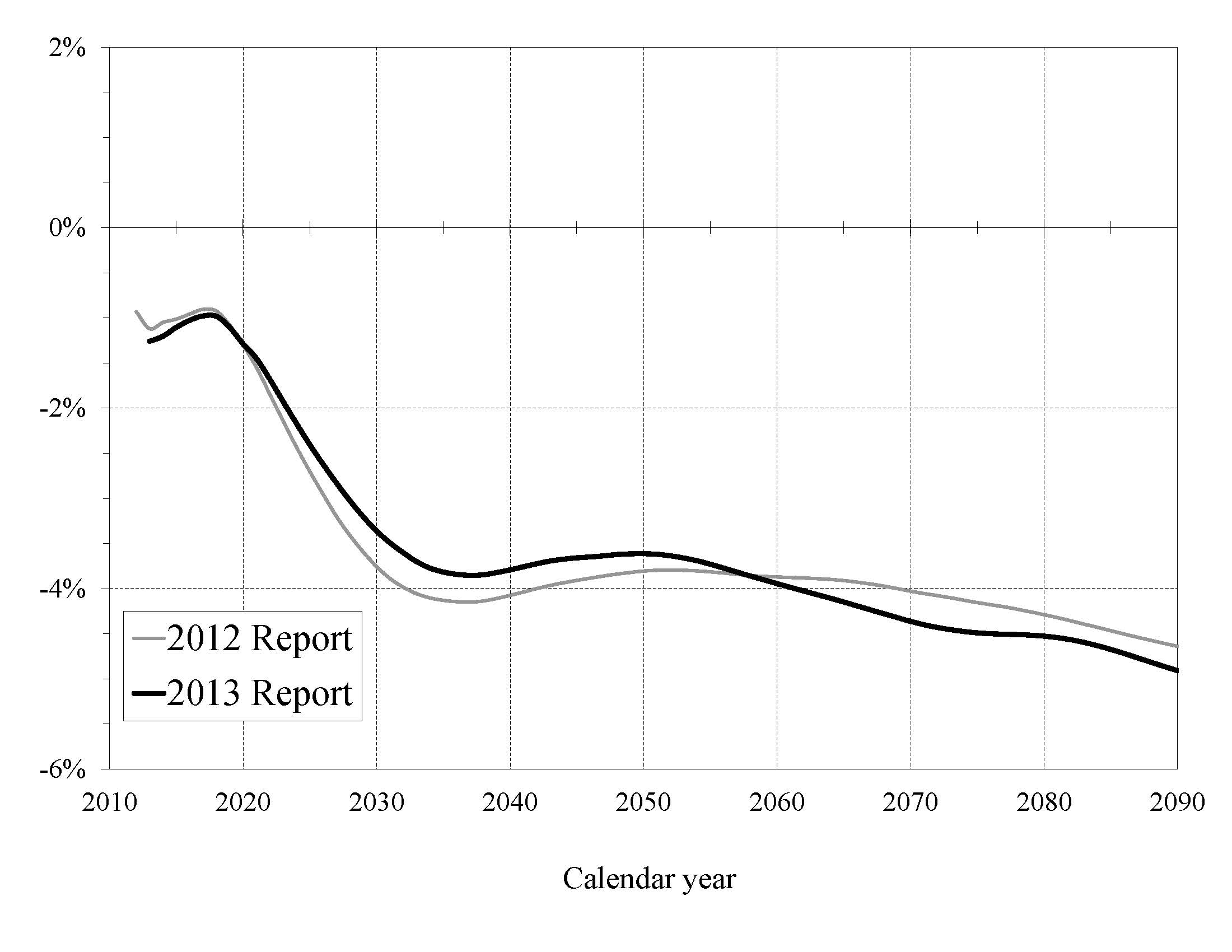

Figure II.D8 compares this year’s projections of annual balances (non-interest income minus cost) to those in last year’s report. See page 76 for details.

|

|

|

|

|

|

|

| SSA Home | Privacy Policy | Website Policies & Other Important Information | Site Map | Actuarial Publications | May 31, 2013 | |