This appendix presents estimates of the probability that key measures of OASDI solvency will fall in certain ranges, based on 5,000 independent stochastic simulations. Each simulation allows key variables to vary throughout the long-range period. These key variables include total fertility rates, changes in mortality rates, new arrival lawful permanent resident (LPR) and other-than-LPR immigration levels, rates of adjustment of status (from other-than-LPR to LPR), rates of legal emigration (from the population of citizens and LPRs), changes in the Consumer Price Index, changes in average real wages, unemployment rates, trust fund real yield rates, and disability incidence and recovery rates. The fluctuation of each variable over time is simulated using historical data and standard time-series techniques. Generally, each variable is modeled using an equation that: (1) captures a relationship between current and prior years’ values of the variable, and (2) introduces random variation based on variation observed in the historical period. For some variables, the equations also reflect relationships with other variables. The equations contain parameters that are estimated using historical data for periods from about 20 years to over 100 years, depending on the nature and quality of the available data. Each time-series equation is designed so that, in the absence of random variation over time, the value of the variable for each year equals its value for the intermediate scenario.

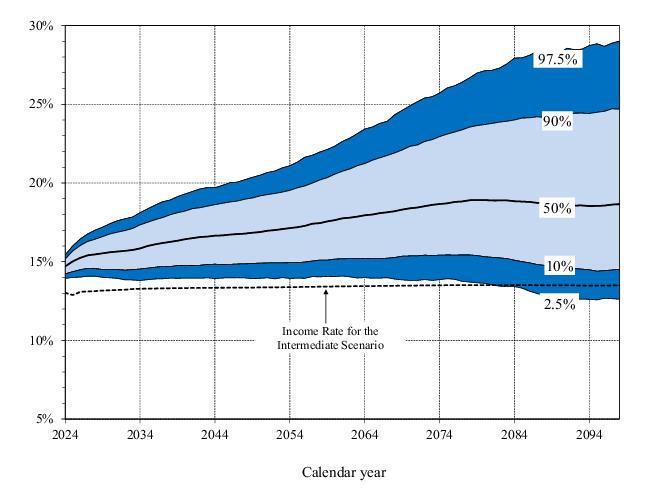

1Figure VI.E1 displays the probability distribution of the year-by-year OASDI cost rates (that is, cost as a percentage of taxable payroll). The range of the annual cost rates widens as the projections move further into the future, which reflects increasing uncertainty. The figure includes only the income rate for the intermediate scenario rather than the probability distribution of the year-by-year income rates, because there is relatively little variation in income rates across the 5,000 stochastic simulations. The two outermost cost rate lines in this figure indicate the range within which future annual cost rates are projected to occur 95 percent of the time. In other words, the current model estimates that there is a 2.5 percent probability that the cost rate for a given year will exceed the upper end of this range and a 2.5 percent probability that it will fall below the lower end of this range. Other lines in the figure delineate the range within which future annual cost rates are projected to occur 80 percent of the time and the median cost rate. The median (50th percentile) cost rate for each year is the rate for which half of the simulated outcomes are higher and half are lower for that year. These lines do not represent the results of individual stochastic simulations. Instead, for each given year, they represent the percentile distribution of annual cost rates based on all stochastic simulations for that year.

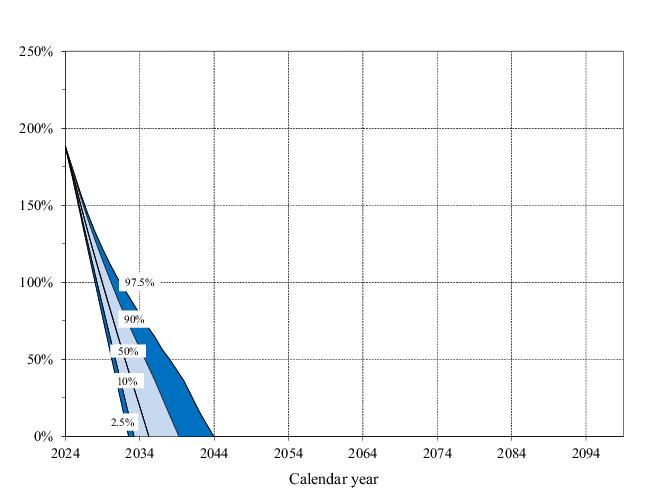

Figure VI.E2 presents the simulated probability distribution of the annual trust fund ratios for the combined OASI and DI Trust Funds. The lines in this figure display the median set (50th percentile) of estimated annual trust fund ratios and delineate the 95‑percent and 80‑percent ranges estimated for future annual trust fund ratios. Again, none of these lines represent the path of a single simulation. For each given year, they represent the percentile distribution of trust fund ratios based on all stochastic simulations for that year.

Figure VI.E2 shows that for 95 percent of the stochastic simulations, the trust fund reserve depletion year falls in the range from 2032 to 2043, relatively early in the 75‑year projection period. The figure also shows that there is a 50‑percent probability of trust fund reserve depletion by the end of 2035 (the median reserve depletion year). The median reserve depletion date is early in 2035; the reserve depletion date for the intermediate scenario is in mid-2035.

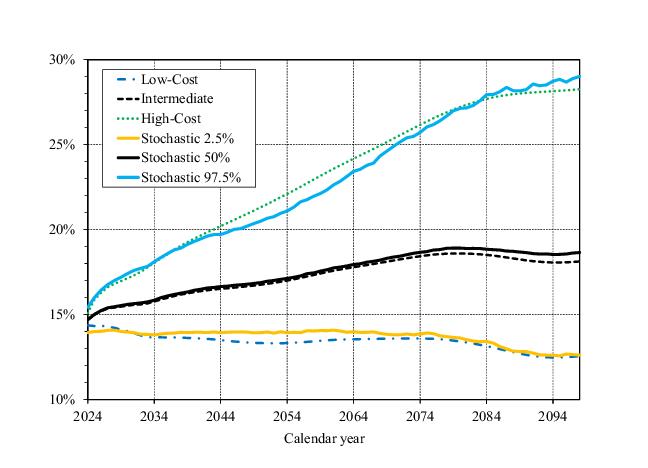

One fundamental difference relates to the presentation of distributional results. Figure VI.E3 shows projected OASDI annual cost rates for the low-cost, intermediate, and high-cost alternative scenarios along with the annual cost rates at the 2.5th percentile, 50th percentile, and 97.5th percentile for the stochastic simulations. While all values on each line for the alternative scenarios are results from a single specified scenario, the values on each stochastic line may be results from different simulations for different years. The one stochastic simulation (from the 5,000 simulations) that yields results closest to a particular percentile for one projected year may yield results that are distant from that percentile in another projected year.

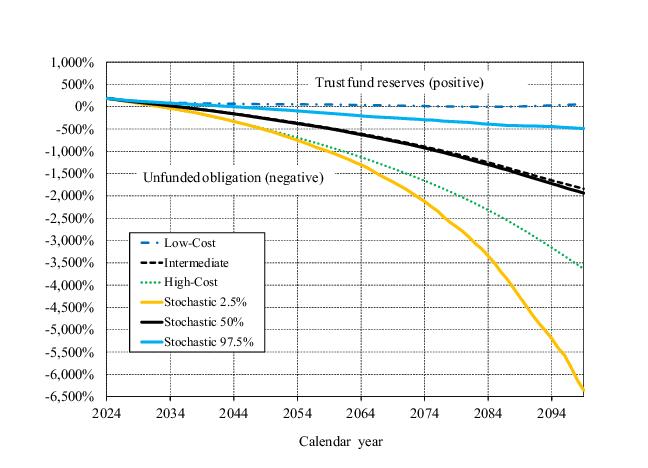

Figure VI.E4 compares the ranges of trust fund (unfunded obligation) ratios for the alternative scenarios to the 95-percent range of the stochastic simulations. This figure extends figure

VI.E2 to show unfunded obligation ratios, expressed as negative values below the zero percent line. An unfunded obligation ratio is the ratio of the unfunded obligation accumulated through the beginning of the year to the cost for that year.

Table VI.E1 displays long-range actuarial estimates for the combined OASDI program using the two methods of illustrating uncertainty: alternative scenarios and stochastic simulations. The table shows scenario-based estimates for the intermediate, low-cost, and high-cost assumptions. It also shows stochastic estimates for the median (50th percentile) and for the 80‑percent and 95‑percent ranges. Each individual stochastic estimate in the table is the level at that percentile from the distribution of the 5,000 simulations. For each given percentile, the values in the table for each long-range actuarial measure are generally from different stochastic simulations.

The median stochastic estimates displayed in table VI.E1 are similar to the intermediate scenario-based estimates. The median estimate of the long-range actuarial balance is -3.54 percent of taxable payroll, about 0.04 percentage point lower (more negative) than projected in the intermediate scenario. The median estimate for the open-group unfunded obligation is $22.6 trillion, which is equal to the estimate in the intermediate scenario. The median first projected year for which cost exceeds non-interest income (as it did in 2010 through 2023), and remains in excess of non-interest income throughout the remainder of the long-range period, is 2024. This is the same year as projected in the intermediate scenario. The median projected date at which trust fund reserves first become depleted is early in 2035; the reserve depletion date for the intermediate scenario is mid-2035. The median estimates of the annual cost rate for the 75th year of the projection period are 18.65 percent of taxable payroll and 6.26 percent of gross domestic product (GDP). The comparable estimates in the intermediate scenario are 18.12 percent of payroll and 6.10 percent of GDP.

For three measures in table VI.E1 (the actuarial balance, the first projected year cost exceeds non-interest income and remains in excess through 2098, and the first year trust fund reserves become depleted), the 95‑percent stochastic range falls within the range defined by the low-cost and high-cost scenarios. For the remaining three measures (the open-group unfunded obligation, the annual cost in the 75th year as a percent of taxable payroll, and the annual cost in the 75th year as a percent of GDP), one or both of the bounds of the 95‑percent stochastic range fall outside the range defined by the low-cost and high-cost scenarios.