|

| The Trustees of the Social Security Trust Funds began the practice of issuing an Annual Report in 1941. This first Report, however, was never published. It was transmitted to the Speaker of the House and the President of the Senate as a letter from the Trustees, and it was never subsequently published either by the Congress or the Social Security Board. We are therefore publishing it here for the first time. |

LETTER OF TRANSMITTAL

Board of Trustees of the

Federal Old-Age and Survivors

Insurance Trust Fund,

Washington, D.C.

January 3, 1941

Sir:

We have the honor to transmit to you the First Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance Trust Fund, in compliance with the provisions of section 201(b) of the Social Security Act, as amended.

Respectfully,

____________________

_________________________

_______________________

The President of the Senate,

The Speaker of the House of Representatives,

Washington, D. C.

|

Introductory Statement

The Federal old-age and survivors insurance trust fund was created pursuant to section 201 of the Social Security Act Amendments of 1939, approved August 10, 1939. This trust fund became effective on January 1, 1940, and superseded the old-age reserve account established under the Social Security Act of 1935. The trust fund is held by a Board of Trustees composed of the Secretary of the Treasury, the Secretary of Labor, and the Chairman of the Social Security Board, all ex officio. The trust fund so held is available for the payment of old-age annuities and survivors insurance benefits and the necessary expenditures incurred by the Social Security Board and the Treasury Department in the administration of the program. The Secretary of the Treasury is designated as the Managing Trustee.

Resources made available to the trust fund included the securities held by the Secretary of the Treasury for the old-age reserve account, accounts standing to the credit of the old-age reserve account on the books of the Treasury as of January 1, 1940, and interest on the investments. The appropriation to the trust fund for the fiscal year ending June 30, 1941, and for each fiscal year thereafter, are required by section 201 of the Social Security Act, as amended, to be equivalent to 100 percent of the taxes (including interest, penalties, and additions to taxes) received under the Federal Insurance Contributions Act and covered into the Treasury. Interest on and proceeds from the sale or redemption of any securities held by the trust fund are required to be credited to the fund.

The trust fund was in operation for only 6 months of the fiscal year 1940. The transition from the old-age reserve account to the new fund was accomplished in such a manner that the financial operations of the program may be considered as continuous from the active beginning of the old-age insurance program in January 1937 to the end of the fiscal year 1940.

The Social Security Act Amendments of 1939, creating the old-age and survivors insurance trust fund and establishing the Board of Trustees, made other significant changes affecting the financing of the old-age and survivors insurance program. The most important of these changes were: advance in the date of the first payment of monthly benefits from January 1, 1942, to January 1, 1940; modification of coverage provisions to permit workers 65 and over to contribute to the system and to qualify for benefits; increase in the benefits payable in the early years of the program; extension of protection to aged wives and dependent children of beneficiaries and to surviving widows, orphans, or dependent parents of insured workers; and continuance of the 1-percent rate on taxable wages and 1-percent rate on taxable pay rolls for 3 additional calendar years (1940-42.) The expected effect of these modifications was to increase disbursements from the trust fund in the next two or three decades and to reduce contributions during the fiscal years 1940 through 1943.

Since contributions are based on wages and pay rolls in covered employment, the volume of these contributions is mainly dependent upon the level of business and industrial activity. In the first 3 years of collection experience, receipts have fluctuated appreciably with changes in business conditions. Disbursements from the trust fund are also affected by such changes. Experience to date is not yet sufficient to indicate reliably the extent or the nature of the relationships between employment conditions and the amount of benefit disbursements. The amount and total volume of benefit payments are dependent principally upon past and prevailing wage levels, the continuity and volume of employment, the average age of retirement, rates of mortality, and the family responsibilities of the workers. Although decreased employment opportunities may be expected to result in immediate increases in the number of beneficiaries and in the total amount of disbursements, the number of future beneficiaries and the amounts of benefits may decrease. Conversely, increases in wages and employment may be expected to reduce the number of new beneficiaries and the amounts of their benefits immediately but should ultimately increase the number eligible for benefits and the size of their benefits. The promptness of retirement after attainment of age 65 markedly affects benefit disbursements and is itself influenced by benefit amounts, wage rates, and the opportunities for employment.

Other factors, the occurrence of which is impossible to predict, will influence the volume of disbursements from the fund. For example, epidemics and natural disasters will affect disbursements on behalf of survivors of insured persons.

The old-age and survivors insurance trust fund provides a financial margin of safety for the system against the first impacts of unforeseen changes in the upward trend of disbursements as well as against these short-term fluctuations and contingencies. At the end of June 1940 approximately 50 million persons already held social security account numbers and about 42 million workers had made contributions toward benefits under the system. In the future, millions of additional workers will come under the program as they obtain jobs in covered employments. Most of the rights now being accumulated toward benefits by these contributors and insured workers will not mature for many years. Consequently, benefits under the program are expected to increase markedly over a long period. This results from the fact that larger numbers of workers will be eligible and will qualify for benefits and from the expectation that the proportion of the population in ages 65 and over, estimated at 7 per-cent in 1940, may eventually rise to perhaps 14 to 16 percent. Hence the essential assurance of future financial soundness of the system, with its rising rate of disbursement, rests on a graduated increase in contribution rates or provision of income from other sources, or both.

Review of Operations of the Reserve Account,

January 1, 1937, to December 31, 1939

The operations and status of the old-age reserve account from January 1, 1937, to June 30, 1939, have been previously reported to Congress by the Secretary of Treasury in accordance with the provisions of the Social Security Act of 1935. Certain of the statements incorporated in these reports may be summarized here as a background for the report of operations during the fiscal year 1940.

In compliance with the 1935 act, annual appropriations to the old-age reserve account were made by Congress. The Secretary of the Treasury was required to submit annually to the Bureau of the Budget an estimate of the amount of appropriation sufficient, on a reserve basis, as an annual premium for the payments required under title II. Table 1 shows the appropriations for the fiscal years from 1937 through 1940.

Although the 1935 statue did not specify that the annual appropriations to the old-age reserve account be equal to the amount of contributions paid into the system, in practice these appropriations were approximately equivalent to contributions collected, less an allowance for administrative expenses. This practice was based on the approximate correspondence between taxes collected, minus administrative expenses, and the estimated annual premium required for title II benefits computed on a 3-percent reserve basis as specified in the act. In reaching this correspondence, account was taken of uncertainties involved in estimates necessarily based on somewhat arbitrary assumptions and on long-range projections into the future.

Table 1.--Receipts, disbursements, and assets of the old-age reserve account

for specified periods, January 1, 1937, to December 31, 1939 1/

| |

January 1 to

June 30, 1937 |

July 1, 1937, to

June 30, 1938 |

July 1, 1938, to

June 30, 1939 |

July 1, 1939, to

Dec. 31, 1939 |

| Receipts (total): |

$267,261,810.97 |

$515,412,232.89 |

$416,951,054.81 |

$550,000,000.00 |

| Transfers from appropriations 2/ |

265,000,000.00 |

387,000,000.00 |

390,000,000.00 |

268,000,000.00 |

| Balance of appropriation available for transfer 3/ |

--- |

113,000,000.00 |

--- |

282,000,000.00 |

| Interest on investments |

2,261,810.97 |

15,412,232.89 |

26,951,054.81 |

--- |

| Disbursements (total benefit payments): |

26,969.35 |

5,404,062.87 |

13,891,583.23 |

4/ 5,905,193.58 |

| Net addition to the account |

267,234,841.62 |

510,008,170.02 |

403,059,471.58 |

544,094,806.42 |

| Total assets (as of end of period) |

267,234,841.62 |

777,243,011.64 |

1,180,302,483.22 |

1,724,397,289.64 |

| Investments (3-percent special Treasury notes): |

267,100,000.00 |

662,300,000.00 |

1,177,200,000.00 |

1,435,200,000.00 |

| Maturing June 30, 1941 |

264,900,000.00 |

264,900,000.00 |

264,900,000.00 |

264,000,000.00 |

| Maturing June 30, 1942 |

2,200,000.00 |

382,000,000.00 |

382,000,000.00 |

382,000,000.00 |

| Maturing June 30, 1943 |

--- |

15,400,000.00 |

497,400,000.00 |

497,400,000.00 |

| Maturing June 30, 1944 |

--- |

--- |

32,900,000.00 |

290,900,000.00 |

| Unexpended balance: |

134,841.62 |

114,943,011.64 |

3,102,483.22 |

289,197,289.64 |

| To credit of appropriation |

61,810.97 |

113,012,391.44 |

66,121.86 |

282,068,217.77 |

| To credit of disbursing officer |

73,030.65 |

1,930,620.20 |

3,036,361.36 |

7,129,071.87 |

1/ On basis of the Daily Statement of the U.S. Treasury (unrevised).

2/ Appropriations by Congress: available July 1, 1936--$ 265,000,000.00

Appropriations by Congress: available July 1, 1937-- 500,000,000.00

Appropriations by Congress: available July 1, 1938-- 360,000,000.00

Appropriations by Congress: available May 6, 1939-- 30,000,000.00

Appropriations by Congress: available July 1, 1939-- 550,000,000.00

3/ Amounts available transferred in a later period. Appropriation balance for fiscal year 1938 tansferred to fiscal year 1939. Appropriation balance as of December 31, 1939, transferred during period January-June 1940.

4/ Effective August 10, 1939 lump-sum payments to covered workers reaching age 65 were no longer certified. |

Since it was necessary under the 1935 act to estimate appropriations in advance of tax collections, a flexible procedure was adopted. Transfers to the old-age reserve account from the appropriations credit were made monthly. These transfers were periodically adjusted to tax collections.

In addition to the appropriations transferred to the account, the other source of income was interest on investments held by the account. The earnings on investments increased from $2.3 million in 1937 to $27.0 million in 1939, reflecting the increase in the assets of the account.

Throughout the first 3 fiscal years of the program, disbursements from the account consisted exclusively of lump-sum payments to the estates of deceased insured workers and to persons reaching age 65. These lump-sum payments increased from $27,000 in the first 6 months of operation (January 1 to June 30, 1937) to $13.9 million in the fiscal year 1939. Monthly benefits under the original set were not scheduled to begin until January 1, 1942.

The amounts in the account not needed to finance current withdrawals were invested by the Secretary of the Treasury as prescribed in the Social Security Act of 1935. The investments of the account were exclusively in special issues of Treasury notes bearing the 3-percent interest. The amounts of such obligations held at the end of each fiscal year are indicated in table 1.

During the first 6 months of the fiscal year 1940, the financing of the program continued to operate under the provisions of the old-age reserve account. The 1940 Treasury Department Appropriation Act contained an appropriation of $580.0 million for transfer to the old-age reserve account, of which $30.0 million was made available in 1939. Hence, on July 1, 1939, the appropriation available for transfer to the account amounted to $550.0 million. During the first 6 months of the fiscal year, $268.0 million was transferred to the account from the appropriation, and $258.0 million of the transfers was invested. The $10.0 million transfers in excess of investments were deposited with the disbursing officer to provide cash for the payment of benefits.

Although the amended provisions for the payment of benefits did not become effective until January 1, 1940, lump-sum payments to workers attaining age 65 were discontinued on August 10, 1939, when the amending act was approved. Consequently, the amount of payments from the account during the first 6 months of the fiscal year 1940 was decreased. This action reduced the number of cases in which deductions had later to be made from monthly annuities payable to qualified aged workers. Lump-sum death payments continue to be made to survivors or to the estates of covered workers who died before January 1, 1940. The total amount of lump-sum payments from July 1, to December 31, 1939, was $5.9 million.

As indicated in table 1, on December 31, 1939, the last day of operation of the old-age reserve account, there was to its credit $1,724.4 million, including the unexpended 1940 appropriation balance of $282.0 million.

Summary of the Operations of the Trust Fund,

January 1 to June 30, 1940

The Federal old-age and survivors insurance trust fund came into existence on January 1, 1940, as required by the Social Security Act Amendments of 1939. A statement of the operations of the fund from that date to June 30, 1940, is incorporated in table 2. This statement also shows the assets of the fund at the end of the fiscal year 1940.

Receipts of the old-age and survivors insurance trust fund from January 1 to June 30, 1940, included the securities held by the Secretary of the Treasury for the old-age reserve account, and the amounts standing to the credit of the old-age reserve account on the books of the Treasury on January 1, 1940, including the unexpended 1940 appropriation balance. During the 6-month period the unexpended appropriation balance was made available for investment. Since the appropriation for the entire fiscal year 1940 was made, in accordance with the provisions of the Social Security Act of 1935, prior to the enactment of the 1939 amendments, the appropriation provisions of the amended set did not become effective until July 1, 1940. The trust fund was also credited with interest earnings for the year, amounting to $42.5 million. Of this amount, $566,311 represented accrued interest on securities redeemed during the 6-month period.

The total fund is available, as needed, for benefit payments required under title II of the amended act, and for reimbursements for administrative expenses. Benefit payments are paid out of the fund by the Managing Trustee, in accordance with section 205(I) of the Social Security Act, as amended, upon receiving certifications from the Social Security Board. Total benefit payments made from January 1 to June 30, 1940, amounted to $9.9 million.

Table 2.--Receipts, disbursements, and assets of the Federal old-age and survivors insurance trust fund as of June 30, 1940 1/

| Receipts (January 1 to June 30, 1940): |

|

$1,766,886,117.49 |

| Transfers from the old-age reserve account: |

|

|

| Investments |

$1,435,200,000.00 |

|

| Cash with the disbursing officer |

7,129,071.87 |

|

| 1940 appropriation credit |

282,068,217.77 |

|

| Interest on investments |

42,488,827.85 |

|

| Disbursements (January 1 to June 30, 1940): |

|

22,188,161.97 |

| Benefit payments |

9,899,894.97 |

|

| Reimbursements for administrative expense |

12,288,267.00 |

|

| Total assets of fund (receipts less disbursements) |

|

1,744,697,955.52 |

| Total investments held: |

|

1,738,100,000.00 |

| 3 percent old-age reserve account notes |

1,413,200,000.00 |

|

| Maturing June 30, 1941 |

264,900,000.00 |

|

| Maturing June 30, 1942 |

382,000,000.00 |

|

| Maturing June 30, 1943 |

497,400,000.00 |

|

| Maturing June 30, 1944 |

268,900,000.00 |

|

| 2 ½ percent old-age and survivors insurance trust fund notes: |

324,900,000.00 |

|

| Maturing June 30, 1944 |

283,000,000.00 |

|

| Maturing June 30, 1945 |

41,900,000.00 |

|

| Unexpended balance: |

|

6,597,955.52 |

| To credit of fund account |

500,242.33 |

|

| To credit of disbursing officer |

6,097,713.19 |

|

1/ On basis of the Daily Statement of the U.S. Treasury (unrevised). |

The 1939 amendments provide that the Managing Trustee shall pay from the trust fund for each 3-month period the amount of administrative expenses, as estimated by him and the Chairman of the Social Security Board, of both the Treasury and the Social Security Board under titles II and VIII of the Social Security Act and the Federal Insurance Contributions Act. This provision became effective on January 1, 1940. Between that date and June 30, 1940, two repayments for administrative expenses were made, totaling $12.3 million. These reimbursements were approximately 4 percent of contributions collected from January 1 to June 30, 1940.

During the period January 1 to June 30, 1940, new investments amounting to $324.9 million were made for the fund and securities amounting to $22.0 million were redeemed as required to meet current withdrawals for benefit payments and administrative expenses. The new investments were in the form of special old-age and survivors insurance trust fund notes bearing 2.5 percent interest. As a result of these transactions the average interest rate on investments of the trust fund was 2.91 percent on June 30, 1940.

The assets of the old-age and survivors insurance trust fund as of June 30, 1940, were $1,744.7 million.

Statement on the Expected Operation and Status of the Trust Fund

During the Fiscal Years 1941-1945

Estimates of receipts and disbursements on a calendar year basis were presented in the Report of the Committee on Finance of the Senate on H.H. 6635 (S. Rept. 734, 76th Cong., 1st sess.). This report, as well as the Report of the Committee on Ways and Means of the House of Representatives on this bill, cautioned that the estimates presented were subject to a margin of error and that "only after experience has been obtained in paying benefits for several years will we have a better picture of the probable future development of the system."

Experience during the fiscal year 1940--the year in which the payments of monthly benefits began--has been unique in many respects, and is not considered to be representative of operations which may be expected for later years of the program. For various reasons, monthly benefit payments in the initial period have been unusually low. Monthly old-age and survivors benefits were payable in only the last six months of the fiscal year 1940. Monthly benefits to those who had previously received lump-sum payments were reduced by the amounts received under the provisions of the 1935 act. Furthermore, persons aged 65 and over prior to 1937 could qualify for benefits only during the latter part of the period January to June 1940 because they had been excluded from coverage by the provisions of the 1935 Act. Although extensive efforts have been made to acquaint insured persons and their dependents with their rights under the provisions of the act, there was a lag in the presentation of claims during the first period of operation.

Tax collections during the fiscal year 1940 also were not typical. In the first six months of the fiscal year, collections were higher than in previous periods because of the taxation retroactively to January 1, 1939, of wages of persons 65 and over enabled by the amendments of 1939 to qualify toward benefits. Other amended coverage provisions became effective on January 1, 1940, thus affecting tax liability in the last six months of the fiscal year and collections in only the last quarter of the fiscal year.

Business conditions which will be reflected in the future operations of the old-age and survivors insurance system may be dependent to a large degree upon the state of international affairs and the domestic armament program. In addition to uncertainties concerning pay rolls and employment, as they affect the volume of contributions paid into the old-age and survivors insurance system, there are also marked uncertainties as to the effects of unusual circumstances upon the promptness of retirement of aged workers, the dependency of other persons as insured workers, and other factors. It is not possible to forecast with confidence the employment opportunities for aged workers, their distribution among various industries, and the effect of the defense program on different industrial groups. If aged workers who are insured remain in covered employments and additional persons in the upper ages obtain such employment, then upon a reversal of those tendencies, their subsequent retirements would occasion a sharp increase in the benefits.

The estimates contained in the reports of the Congressional committees referred to above continue to furnish a useful guide to the in rates of retirement and mortality. Because of these factors, a range of from $5,000 million to $7,000 million in the estimate of the trust fund at the end of fiscal year 1945 may be regarded as reasonable.

Table 3.--Estimates of operations of the Federal old-age and survivors insurance trust fund, fiscal years 1941-45

(Subject to the limitations stated in the text)

(In millions)

| |

Fiscal year

|

| |

1941 |

1942 |

1943 |

1944 |

1945 |

| Fund at beginning of year |

$1,745 |

$2,363 |

$2,965 |

$3,653 |

$4,775 |

| |

| Transactions during year: |

| Appropriations (taxes) |

667 |

725 |

906 |

1,450 |

1,450 |

| Interest on investments |

56 |

71 |

86 |

105 |

128 |

| Total income |

723 |

796 |

992 |

1,555 |

1,578 |

| Benefit payments |

78 |

165 |

274 |

402 |

548 |

| Administrative expenses |

27 |

29 |

30 |

31 |

32 |

| Total disbursements |

105 |

194 |

304 |

433 |

580 |

| Net increase in fund |

618 |

602 |

688 |

1,122 |

998 |

| |

| Fund at end of year |

2,363 |

2,965 |

3,653 |

4,775 |

5,773 |

Actuarial Status of the Trust Fund

The uncertainties as to tax income and benefit outgo during the next few years have been outlined in the preceding section. In considering the actuarial aspects of operations in the longer future, the unreliability of any specific estimates is of such degree that only the general course of financial development of the program may be indicated. It is possible to demonstrate the assured upward trend in benefit disbursements and the relation of this trend to an income base, admittedly artificial as a guide to the future but derived from the present wage and employment pattern, from an "intermediate" estimate of population growth, and free from the graduated tax increases of the Federal Insurance Contributions Act. Short-term changes in business conditions or employment will cause substantial variations from the trend. Furthermore, basic changes in the economy, such as altered productivity or new lines of industrial pursuits, as well as changes in mortality rates, dependency and other factors may occur which may cause the actual experience to vary significantly from any specific projections.

The numerous influences on future cost which are potential in a system of this magnitude and complexity, and in a program with such inherent interplay within the life pattern of more than one-half of our population, were indicated to Congress on pages 2473-2488 of the "Hearings Relative to the Social Security Amendments of 1939 Before the Committee on Ways and Means, House of Representatives, Seventy-sixth Congress." These numerous factors of affecting costs are not susceptible of effective revaluation within a short period of time. Consequently, it is the opinion of the Board of Trustees that no better basis for illustrations of long-range trends can at this time be adduced than that which rests upon the assumptions outlined in the above citation.

Illustrations of future cost possibilities must recognize an upward trend in benefit outgo for long periods ahead. The amendments of 1939 greatly improved the protection afforded covered groups in the population by bringing monthly benefits to widows and children of deceased covered workers. These new protections, while of major significance to the security of insured workers and their families, represent only about one-fourth of the costs of the program; the remaining portion of the disbursements is for old-age protection. This is significant since, with a larger number and percentage of the population at ages above 65 definitely anticipated for the future, the number of qualified beneficiaries may be expected to increase more or less steadily for perhaps a century.

The actuarial status of the trust fund may be measured by a variety of methods. One method is to estimate the income and disbursements of the fund during specified future periods as shown by table 4, according to which annual tax collections would be expected to rise from an average of almost $1 billion for the first 5 years of operation under the amended set to an average of $1.7 billion during the second 5 years of operation and to approximately $2.5 billion 35 or 40 years hence.

Annual benefit payments may be expected to increase from an average of about $0.3 billion for the first 5 years to almost $1 billion for the second 5 years. After a 40-year period, average annual benefit payments may have risen to a magnitude of about $3.5 billion and, after a 50-year period to over $4 billion. A further rise after that period may be expected because of the anticipated increase in the number of persons qualifying for benefits and in the average benefit payments.

Table 4.--Estimated average annual benefit payments and tax income of the Federal old-age and survivors insurance trust fund for future quinquennial periods, fiscal years 1941-90 1/

(Subject to the limitations stated in the text)

(In billions)

Fiscal year

period |

Average annual

benefit payments |

Average annual

tax income |

1941-45 |

$0.3 |

$1.0 |

1946-50 |

0.9 |

1.7 |

1951-55 |

1.5 |

2.0 |

1956-60 |

1.9 |

2.1 |

1961-65 |

2.4 |

2.2 |

1966-70 |

2.8 |

2.3 |

1971-75 |

3.1 |

2.4 |

1976-80 |

3.5 |

2.5 |

1981-85 |

3.9 |

2.6 |

1986-90 |

4.1 |

2.6 |

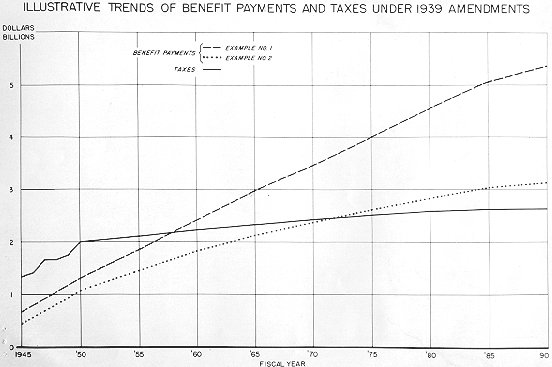

1/ The figures in this table after the first quinquennial period are based on the chart; the benefit-payment figures represent the average of the two examples given there. Figures for the first quinquennial period are based on table 3.

The accompanying chart illustrates by two examples the possible trend over a 45-year period (1945-90) of future contribution income and future benefit payments. The range in the benefit figures shown in the chart does not represent minimum or maximum values. The examples are merely illustrative of reasonable projections. The values upon which this chart is based are those discussed by the Actuarial Consultant of the Social Security board in the Hearings of the Committee on Ways and Means previously cited.

As indicated in the chart, throughout the initial period taxes exceed benefits. This would result in a fund accumulation which provides interest earnings to meet a portion of the current benefit payments. If disbursements and collections under the program should follow the growth curve of example 2, benefits would begin to exceed taxes within 35 years; but because of the interest earnings of the fund, total annual income might continue to exceed annual benefits indefinitely. If, however, future experience should more closely approximate the curve of example 1, benefits would exceed taxes within approximately 20 years and would exceed the sum of taxes and interest on the fund within the following 5 years; and since the prior accumulation in the trust fund under the conditions of this example would cover excess disbursements for only a limited period, additional income would eventually be required. Because of the cumulative growth of the disbursements, any long-term deficiency in the finances of the program would be apparent well in advance, and, therefore, could be met without serious shock or disturbance, by moderate changes in the financial provisions.

Expected Relations Between Size of the Trust Fund and Disbursements

On the basis of present estimates it is apparent that during the ensuing five fiscal years the trust fund will exceed three times the highest annual expenditures anticipated during that five-fiscal-year period. This condition is reported at this time to the Congress in accordance with section 201(b)(3) of the Social Security Act.

The primary consideration with respect to the size of the trust fund is its role in relation to the financial integrity of the social insurance program. In addition, the Board of Trustees must have regard for the relationship of the fund to the fiscal position of the Government and the economic position of the Nation.

The present low level of current disbursements may be increased sharply with a change in employment conditions within the next few years; nor is this level representative of what is likely to be the long-term experience. The probable future level of benefit payments is high and the trend of such payments will be steeply ascending over the next generation and longer. The actuarial analysis discussed on pages 14-17 indicates that a generation hence disbursements will be at least three to four times greater than the maximum disbursements which may be expected in the next five fiscal years. Prudent management, therefore, requires emphasis on the long-range consideration of income and disbursements.

Having regard for these long-range as well as for short-range commitments and for fiscal and economic relationships, the Board believes that the trust fund is not excessive in size.

Summary and Conclusion

In presenting this report to Congress in accordance with section 201(b) of the Social Security Act, as amended, the Board of Trustees reports that the purposes to be served by the amendments of 1939 have been safeguarded in every respect.

The essential function performed by the old-age reserve account have been taken over by the new trust fund. These functions are strengthened and the interests of the beneficiaries emphasized by the modification of procedure under which appropriations to the fund are now related directly to the tax collections.

During the six months of operation of the old-age and survivors insurance trust fund (January 1 to June 30, 1940), receipts of the fund, including the investments held by and amounts credited to the old-age reserve account, the transfers from the 1940 appropriation balance, and interests on investments, totaled $1,766.9 million. Disbursements from the fund for benefit payments and reimbursements for administrative expenses were $22.2 million. On June 30, 1940, assets of the trust fund amounted to $1,744.7 million of which $1, 738.1 million represented investments.

The trust fund augmented by the anticipated income of the next five fiscal years is ample to assure the payment of benefits and administrative expenses for this period. However, the next five-year period is but the introduction to several generations during which the trend in benefits, while predictable in degree, will be pronouncedly upward.

The future benefits to which we are now committed will require large scale outlays many times greater than the level of payments in the first five years. Expected income will also be increasing, but whether or not additional income will be needed in the long-distant future cannot be determined at this time. In view of the short period during which the amended act has been in force and the magnitude of the long-range commitments of the program, the Board makes no recommendation at this time for changing the tax rates under sections 1400 and 1410 of the Federal Insurance Contributions Act.

|