Statement of Stephen C. Goss,

Chief Actuary

Social Security Administration

Testimony before the House Committee on Ways and Mean, Subcommittee on Social Security

March 22, 2016

Chairman Johnson, Ranking Member Becerra, and members of the subcommittee, thank you very much for the opportunity to speak to you today about the way Social Security benefits are adjusted currently for workers with earnings not covered under the program, and recent proposals to modify this adjustment. I will focus on the effects on Social Security beneficiaries of H.R. 711, introduced by Chairman Brady with Representative Neal on February 4, 2015, and the proposal included in the President's Fiscal Year 2017 Budget. Each of these proposals included modifications of the Windfall Elimination Provision (WEP) that applies to primary benefits for retired-worker and disabled-worker beneficiaries, as well as to auxiliary benefits for their spouses and children. Please refer to our enclosed letters providing estimates of the implications of these proposals for Social Security actuarial status, which are also available at https://www.ssa.gov/oact/solvency/index.html.

Present Law Windfall Elimination Provision (WEP)

Under current law, retired-worker and disabled-worker beneficiaries have their primary insurance amount (PIA) computed with a three-segment formula, which applies a 90 percent factor to the lowest portion of their average earnings, 32 percent to a substantial “middle” portion of their average earnings, and 15 percent to the highest portion of earnings for high earners. Average earnings are computed reflecting the highest 35 years of covered earnings for most retirees, and fewer years included for most disabled workers. Career-average covered earnings for workers who have some non-covered earnings are generally lower than career-average covered earnings for similar workers who worked solely in covered employment. Therefore, a higher proportion of average covered earnings are in the lower PIA formula bracket, and in turn, the PIA formula provides a higher “replacement rate,” (that is, the ratio of PIA to career-average indexed earnings) for these workers than for similar workers who worked solely in covered employment.

In order to offset the advantage, or windfall, provided in the PIA formula for workers with non-covered earnings, the WEP gradually reduces the 90 percent PIA factor used for beneficiaries with 30 or more years of substantial covered earnings to 40 percent for those with 20 or fewer years of substantial covered earnings.. A similar adjustment is applied for disabled worker beneficiaries with non-covered earnings.

The WEP is limited in application so that it does not reduce the PIA by more than one-half of the amount of the retirement or disability pension (periodic payment) received by the worker based on non-covered employment. Worker beneficiaries who are not known to be receiving periodic payments based on their non-covered earnings do not have their PIA reduced by the WEP.

Proposed Change in WEP for Worker Beneficiaries Newly Eligible in the Future

The proposal introduced by Chairman Brady and Representative Neal (H.R. 711) and the proposal included in the President’s Fiscal Year 2017 Budget would ultimately alter the adjustment of worker primary benefits in the same way, starting with those newly eligible for worker benefits in 2017 for H.R. 711 and in 2027 for the President's proposal. This new adjustment would effectively apply the benefit replacement rate the worker would have had if all of his or her earnings had been covered under the Social Security program, to the worker's average indexed monthly earnings (AIME) using only covered earnings on which payroll taxes were paid.

Adjusted PIA = ( PIA using all earnings / AIME using all earnings ) * AIME using covered earnings only

This adjustment would be applied whether or not the worker is eligible for or receiving a pension based on non-covered earnings, and does not include a limitation based directly on the number of years of substantial covered earnings (in other words, the 30-years-of-coverage exclusion is eliminated). Because the Social Security Administration has records of non-covered earnings for years after 1977, but does not have universal access to records for receipt of non-covered pensions, this new adjustment would be much easier to apply, and would be applied much more uniformly to all workers with some years of non-covered earnings.

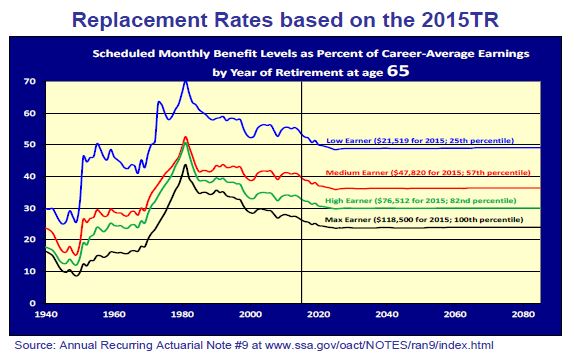

The figure below illustrates how the benefit replacement rate varies for retired-worker beneficiaries (retirees starting benefits at age 65) depending on the level of their career-average covered earnings.

For example, a worker with career-average earnings of $47,820, our “medium earner,” receives a retirement benefit of about 40 percent of their career-average earnings. However, if the same worker happens to have worked in non-covered employment for a little over half their career, such that their career-average covered earnings are only at $21,519, the level for our “low earner,” then the benefit will be about 53 percent of the career-average covered earnings. While the current WEP attempts to adjust for this disparity, the variability in pensions based on non-covered earnings and the reporting of these pensions leads to inconsistent adjustments in benefit levels.

The change proposed in H.R. 711 and in the Fiscal Year 2017 Budget makes a direct adjustment to the replacement rate such that the worker described above (overall career-average earnings at the medium-earner level, with a little over half of the earnings in non-covered employment, so that their career-average covered earnings would be at the low–earner level) would receive a benefit replacement rate of 40 percent, instead of 53 percent. This adjustment would occur uniformly and consistently for individuals with split careers between covered and non-covered earnings. Differences in pension levels and reporting by various non-covered employers would no longer influence the adjustment to Social Security worker benefits. The implicit rationale for this approach may be characterized as: for years of non-covered earnings, where neither the employer nor the employee paid Social Security payroll tax, the employee and employer should be responsible for providing pension coverage and disability protection.

Ultimate Effects on Beneficiaries of the New WEP Adjustment

In order to meaningfully illustrate the effects of the new adjustment on workers who will become eligible starting in 2017 and 2027, respectively, under these proposals, we provide estimates of the effects of the new adjustments on all current beneficiaries in 2016, as though the new approach applied to them. The average monthly WEP reduction for workers in 2016 with the current approach is about $270.

For the roughly 1.5 million retired-worker and disabled-worker beneficiaries in 2016 whose primary benefit is reduced under the current WEP, the new adjustment would result in an increased primary benefit for about 1.25 million beneficiaries (about 84 percent of all currently-affected beneficiaries). The average reduction would be about $77 less on average, from $274 per month under the current WEP to about $198 per month under the new adjustment. The remaining 0.25 million beneficiaries (about 16 percent of all currently-affected beneficiaries) would see a further small reduction in their primary benefit. Their average reduction would be about $13 more on average, from $190 per month under the current WEP to about $203 per month under the new adjustment.

For 2016, we estimate that there are roughly 15 million retired-worker and disabled-worker beneficiaries with some non-covered earnings after 1977 who are not reduced under the current WEP. We estimate that for about 1 million (about 7 percent) of these beneficiaries, the new adjustment (if it were in place in 2016) would not change their primary benefit. For the other 14 million beneficiaries, the average reduction in benefit would be about $27 per month for 2016. For the half of this 15 million least affected by the new adjustment, the average primary benefit reduction would be just $3 per month. For the half most affected, the reduction would average $46 per month. About 55 percent of the 15 million, or roughly 8 million beneficiaries, qualify for exemption from the current WEP because they have 30 or more years of substantial covered earnings. Because these 8 million retired-worker or disabled-worker beneficiaries have relatively few years of non-covered earnings, their reduction under the new approach would be relatively small. In addition, more than 75 percent of these 15 million workers have fewer than 5 years with any non-covered earnings.

Proposed Change in WEP for Worker Beneficiaries Newly Eligible in the Past or Near Future

Both proposals would expand the application of the current WEP to worker beneficiaries first eligible before the implementation of the new adjustment formula.

Under H.R. 711, all individuals eligible for retired-worker or disabled-worker benefits for December 2016 who: (1) have any recorded non-covered earnings after 1977, (2) are not currently affected by the WEP, and (3) have less than 30 years of substantial covered earnings, would be required to obtain by the end of 2016 certification from any employer who paid him or her non-covered earnings. This certification would indicate whether the worker is vested for a pension, and when and how much pension has been received. A WEP reduction would be applied if it is determined to be warranted for past or future benefits. If the WEP reduction is applicable for past benefits, an overpayment would be established to be repaid by the beneficiary, principally through recovery from his or her future benefits. If an individual does not obtain certification, then the WEP would be applied for past and future benefits limited only by the number of substantial years of covered earnings.

Under H.R. 711, a “rebate” would be applied for all benefits reduced by the current WEP based on entitlement for months in 2017 and later. The rebate would be determined to be as high as possible, but not in excess of 50 percent of the WEP reduction, and limited to assure that the net effect of the Bill on Social Security program cost through 2025 would be neutral or positive. We estimate that the maximum permissible rebate percentage of 50 percent would be applicable.

Under the President's proposal in the 2017 Budget, employers would be required to report all periodic payments (pensions) based on non-covered earnings for past and future years, for workers who were or will be first eligible for a retired-worker or disabled-worker benefit before 2027. This additional reporting, particularly from state and local governments, will lead to additional workers being subject to WEP reduction for past and future benefits.

Effects on Beneficiaries of the Increased Application of the Current WEP

Under H.R. 711, we estimate that up to 10 percent of the 7 million worker beneficiaries in December 2016 with some past non-covered earnings, fewer than 30 years of substantial covered earnings, and no current WEP reduction would be determined to warrant a WEP reduction on some past or future benefits. This assumption is very uncertain, and the actual number would depend substantially on the efforts made by beneficiaries and their former employers to produce and obtain valid certification of their pension vesting and payments received. We estimate that for this group, the average amount of overpayment made before 2017 that would be recovered in 2017 through 2025 will be roughly $8,000. For future benefits to this group, the average total benefit reduction through 2025, net of the 50-percent rebate, will also be roughly $8,000. Recovery of overpayments for prior months would be limited by the financial status of the beneficiaries and the remaining duration of their benefit receipt. Thus, the number of individuals with recovery and reduction of benefits is very uncertain.

Under the President's proposal, we estimate that establishing systems for reporting of pension payments based on non-covered earnings would require about 3 to 6 years to fully develop and would ultimately capture most but not all non-covered pension recipients. We estimate that the percentage of the 7 million worker beneficiaries in December 2016 with past non-covered earnings, fewer than 30 years of substantial covered earnings, and no current WEP reduction who would be determined to warrant a WEP reduction on some past or future benefits under the President’s proposal would be significantly lower than for the process under H.R. 711. In addition, because reductions and recoveries would be applied only for months with verified receipt of pension payments and would be limited based on the size of the pension payments, the average reduction or recovery might be smaller per month than under H.R. 711. Overall, we estimate that program savings through 2025 for benefit reductions and recoveries under the President’s proposal for worker beneficiaries entitled for December 2016 would be less than half the amount expected under the provisions of H.R. 711. Under the President’s proposal, however, additional workers becoming newly eligible for retired-worker or disabled-worker benefits after December 2016, through 2026, would also be found to have non-covered pension payments requiring application of the WEP adjustment.

Government Pension Offset (GPO)

The President's proposal would utilize the additional reported pension data to improve application of the current law GPO. The proposal would also change the GPO provision for those eligible after 2026, limiting the offset to spouse benefits (including divorced and surviving spouses) at age 62 or older and to spouse benefits for those also receiving any Social Security benefit based on their own disability (including disabled worker, disabled widow, and disabled adult child beneficiaries under age 62). The offset would be applied to these auxiliary benefits more consistently, based on their past earnings in non-covered employment. The new offset would reduce the amount of the auxiliary benefit by the excess of (1) the auxiliary beneficiary's own potential retired-worker or disabled-worker benefit based on all of his or her earnings over (2) the auxiliary beneficiary’s potential worker benefit based on covered earnings only. This excess amount would be calculated and applied regardless of the insured status of the auxiliary beneficiary. This provision contributes to the program savings under the President's proposal as indicated in our letter to the Director of OMB. It is our understanding that the intent of this hearing is to explore proposals affecting the WEP adjustments on primary benefits for workers, so I will not cover the details of the GPO provisions in this testimony.

Conclusion

Both H.R. 711 and the President's proposal in the Fiscal Year 2017 Budget would ultimately result in a more consistent and logical adjustment to the primary benefit amounts for workers with career earnings split between covered and non-covered employment. The analysis offered here reflects intense analytical work by several people in our office, but particularly Jacqueline Walsh and Bert Kestenbaum (now retired). We appreciate the opportunity to share the results of our analysis and our estimates for the effects of these proposals. They are, as always, a work in progress. I will be happy to attempt to answer any questions you may have.

Stephen C. Goss response to Chairmen Brady

Stephen C. Goss response to OMB Director Donovan